by Devon Wilson | Mar 13, 2023 | Credit Union Solutions

Credit unions are a great resource for those looking to save money on banking services while also making a positive impact on the local community. As we move further into the decade, it’s important to stay up to date on the trends in credit unions that...

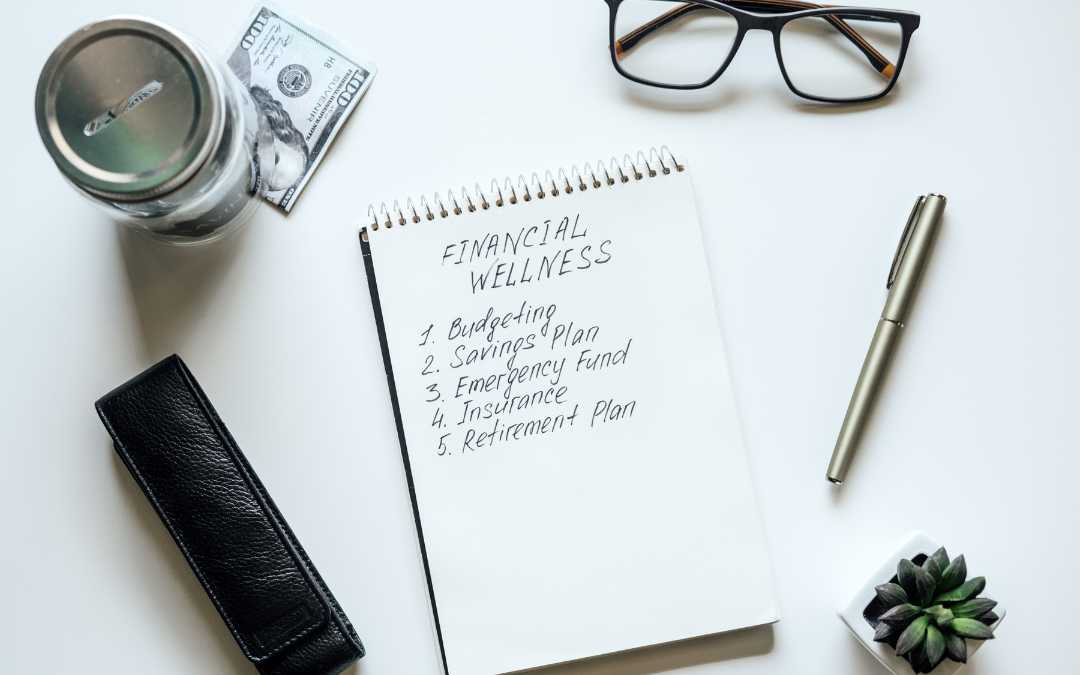

by Devon Wilson | Mar 6, 2023 | Marketing

Two-thirds of adults in the U.S. say that money is a significant source of stress in their lives, according to the American Psychological Association. And money-related stress is more prevalent in younger adults, which means it’s time to start talking about...

by Devon Wilson | Nov 1, 2022 | Credit Union Solutions

Autumn is a season of change and preparation. The holidays are right around the corner, the summer vacations are all long since passed, and it’s time to start thinking about the new year. For your credit union members, autumn banking trends can be cyclical –...

by Devon Wilson | May 9, 2022 | Credit Union Solutions

Recently, the Credit Union National Association held its annual governmental affairs conference. They covered a wide range of topics from regulatory changes to future initiatives and more. After the conference, American Banker compiled a list of 6 topics from...